Several recent commentaries and reports were drafted in the mean time. The Centre for European Policy Studies let us know in the commentary 'Banking Union in the Eurozone

and the European Union' that there is a need, to start with, to distinguish clearly what is needed to address a‘systemic’ confidence crisis hitting the banking system – which is mainly or solely a

eurozone problem – and ‘fair weather’ arrangements to prevent individual bank

crises and, when they occur, to manage them in an orderly fashion so as to minimise

systemic spillovers and the cost to taxpayers, which is of concern for the entire

European Union. Much of the ongoing debate on deposit insurance and banking

resolution funds mainly refers to the latter issue.

In the recent drafted report 'Completing the Euro', in the chapter on 'Banking and the financial sector' a euro area banking union is pledged. Financial market stability has been neglected by the architecture of the

Maastricht Treaty. Despite an increasingly integrated EU financial market,

with the volume of cross-border banking growing substantially in the 2000s,

financial supervision remained a prerogative of Member States, with only a

modest degree of supranational coordination. This dichotomy prevented, prior

to the crisis, both the detection of the development, in some EU countries, of

excessive private sector imbalances and the identification of cross-country and

cross-sector interlinkages, which therefore went unaddressed. In addition to

these banking supervision deficiencies, the EU faced the financial crisis with

no banking crisis management capacity.

The lack of a European framework for banking supervision and crisis resolution

is, at least partly due to the fact that, until the crisis, the interdependency

between national banking systems in the EMU was underestimated. The crisis

has highlighted the fact that, given the increased financial integration spurred

by the common currency, the financial instability faced by one Member State

is a threat for the EMU as a whole. Furthermore, the crisis exposed a fragility

of the euro area, which is the interconnection between the banking crisis and the sovereign crisis that weaken both sovereigns and banks and the whole monetary union as a consequence.

As the failure of financial markets is at the heart of the crisis, a comprehensive framework for financial stability is a crucial piece in the EMU (Economic Monetary Union) puzzle. This implies moving towards a banking union addressing the financial system deficiencies revealed by the crisis

|

|

Although it would seem straightforward to establish a banking union for the EU as a whole because of the character of the single financial market as an EU-27 feature, we consider that the euro area should not wait for an agreement in the EU-27 framework and not make any concession in order to move to an EU-27 framework if that entailed a less functional solution for the euro area.

We therefore call upon the euro area to take the lead in the setting up of a true banking union. We are aware that it could be a delicate issue to achieve the right rules for financial stability in the euro area without endangering the functioning of the single financial market. But it must be possible to ensure that the banking union within the euro area do not entail distortions to competition between the EU-27 within the single market for financial services and the euro area.

The recent reforms in EU financial market supervision

are not sufficient. Following the crisis, the EU supervisory framework already underwent a comprehensive reform, aimed at ensuring a stable, reliable and robust single market for financial services. The new architecture consists of two mutually reinforcing European pillars. On the one hand, a micro-prudential pillar, with the establishment of three European Supervisory Authorities (ESAs) for banking (EBA), securities (ESMA) and insurance and pension funds (EIOPA). The specific powers granted to the three ESAs have been designed to improve the quality and consistency of supervision, reinforce the supervision of cross-border groups, strengthen crisis prevention and management across the EU, and establish a set of common standards applicable to all financial institutions. On the other hand, a macro-prudential pillar, with the creation of the European Systemic

Risk Board (ESRB) with a mandate to prevent and mitigate the build-up of risks

to financial stability in the EU financial system and to contribute to the smooth

functioning of the internal market.

This new framework for financial supervision is a step in the right direction.

However, the design as a coordination framework means that national authorities

will ultimately retain competence for most decisions. Indeed, the new

supervisory agencies have limited powers and resources. The EBA does not

have the power and capacity to conduct deep and far-reaching bank stress tests.

It still has to rely on information provided by national supervisors, who ultimately

have the authority to intervene.

The EBA is thus not yet a true European

supervisor, and even less a euro area supervisor. The limited supervisory role

of the EBA is, of course, related to the absence of financial means at EU level to

support banks in difficulty. Taxpayers’ resources remain firmly in the hands of

national governments and parliaments, and logically therefore Member States

have the main responsibility for banking supervision. |

|

Concerning the ESRB, it has the task of monitoring the soundness of the whole

financial system in the EU; but with more than 60 participating institutions it

is unlikely to become a very effective institution. In addition, it has only access

to aggregate data. If the ESRB wants to obtain information on individual banks,

it has to ask the national supervisors in a complicated process. And even if it

identifies risks, the ESRB can only issue warnings and recommendations which

are not binding for the country to which they are addressed. Furthermore, the

resolution of a cross-border financial institution under the new framework will

still be a highly complex task, as several national authorities, national deposit

insurance funds and national resolution funds will be involved. The reform

undertaken is then insufficient to remedy the problems of financial supervision

and crisis resolution in the EMU.

We need to move towards a more European solution for both banking supervision

and crisis resolution at the EMU level. In designing the EMU banking

union, it is vitally important that future arrangements for supervision and crisis

resolution of cross-border banks are dealt with jointly as a package and not in

isolation, as the solutions in these two areas are totally intertwined. We cannot separate the supervision from the resolution in the sense that supervision is the preventive arm and even if we prevent crises they will still occur and then we will need the corrective arm.

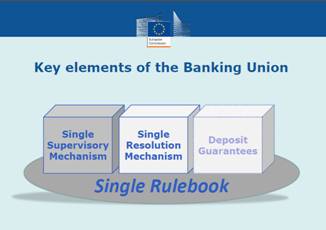

A BANKING UNION FOR THE EURO AREA

The euro area banking union should in the first place include a fully integrated banking supervision for the euro area. This would include having a euro area supervisory institution being responsible for micro prudential supervision with investigation powers. Creating an integrated euro area banking supervisory authority instead of 17 autonomous national supervisors would have obvious advantages compared with the status quo. With integrated supervision, all relevant microeconomic data for euro area banks would be made available to a single institution. This would allow the supervisor to identify all financial links between the Member States, as well as concentrations of lending to specific borrowers, sectors and regions. A euro area institution would be much more independent of national interest groups and politicians than a national supervisor. Thus, the problem of “regulatory capture” could be avoided or at least dramatically reduced.

This euro area banking supervisory institution should either be built up within the ECB or closely cooperate with the ECB. |

|

Conferring specific tasks upon the ECB concerning policies relating to the prudential supervision of credit institutions and other financial institutions, but not insurances could even be done without changing the Treaty. Article 127.6 TFEU allows the Council after consulting the European Parliament and the European Central Bank, to unanimously make that choice.

Overall, the group considers that supervision of banks should, as a general rule, be consistent with the EU internal market rules and seek to avoid regulatory arbitrage between different levels. A pan-EU supervisory authority in a position of hierarchical superiority vis-à-vis national layers of supervision would be the most desirable approach. The exact design would have to be determined politically, in particular with regard to the relationship of euro area countries to the

EU-27 28

A EURO AREA DEPOSIT INSURANCE SCHEME

In parallel to an enhanced supervision structure, there should also be the

setting up of a crisis resolution framework at the euro area level. The euro area

should aim at creating a framework inspired by the Federal Deposit Insurance

Corporation in the US (FDIC), combining the function of a banking resolution

agency and a deposit guarantee scheme. A European FDIC-style agency would

have to become involved at an early stage in the resolution of a cross-border

banking crisis, assuming a role in negotiating the resolution path, alongside

the relevant national authorities. This could include the adoption of ex-ante

burden sharing arrangements. This agency could also supply funds needed

to facilitate the resolution of a cross-border banking group, provided this was

less costly than paying out deposits in liquidation. The euro area-wide bank

deposit guarantee scheme, which would serve as a “pay-out box” in case of

deposit losses, would be easier to implement and less controversial, as public

guarantees on bank deposit across the EU are partially harmonized and less

discretionary.

The costs of a European FDIC-style agency could be based on an insurance fee

raised from the banks, but would clearly have to be complemented with pay-ins

from national budgets. As a system of euro area-wide guarantees as a backstop

would be necessary for both households and non financial corporates deposits,

the amounts involved would possibly be very large. The intervention capacity

would therefore have to be financed and backed up by all euro area governments.

In order to reduce the moral hazard associated with the potential use

of public money, deposit authority should be assigned some “prompt corrective

action mandate” (as the FDIC in the US). One option to discuss could be to

provide the European deposit/resolution authority with the power to monitor

the “recovery and resolution” plans submitted by banks to their primary supervisor.

Moreover, there should be clear rules for the resolution authority to

impose losses to creditors (bail-in instruments). |

.png)