| Paul N. Goldschmidt Director, European Commission (ret.); Member of the Advisory Council of "Stand Up for Europe" wrote May 31st, 2020 (Copyright © 2020 Director European Commission (ret.), All rights reserved):

"The speech of Ursula von der Leyen who presented the Commission's budgetary proposals to the European Parliament for the period 2021-27 struck the right cord both in tone and in content. As in rugby, it is now necessary to "convert the try" and to pull the Union out of the rut in which it is stuck in order to implement a new major step towards European integration.

The crucial idea consists in the willful creation of a financial "transfer" mechanism which – in the light of the significant amounts involved – considerably expands the current limited budgetary framework, overlooks the old disputes over "I want my money back" and ends, at least for the future, the taboo of "debt mutualization". The adoption of this unprecedented framework is still far from assured, but it is crucially important that the modalities of its implementation should avoid, at all costs, compromises that would inhibit the future broadening of the scope to which the new tools available can be put to use.

In the discussion that follows which is somewhat technical – for which I apologize to my non-specialist readers – I draw attention to several notions that seem to me essential if the EU is to take full advantage of these bold proposals. In so doing the EU will demonstrate conclusively, the added value of a common approach to address the challenges that the sanitary crisis has revealed but which clearly extend to many other sectors where a similar logic is applicable (defence, currency, taxes, environment, etc.).

Overall framework:

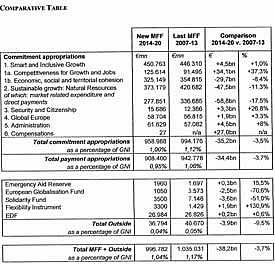

The proposals call for integrating a massive new recovery plan, aimed at the EU 27's battered economies, within the "multiannual financial perspectives2021-27". Its size reaches € 1,850 billion of which €750 billion, financed through borrowings, are specifically dedicated to the recovery effort.

One should point out that the stupendous cumulative amount, in excess of € 6 trillion, announced by the EU, the EMS, the EIB, the Member States and also the ECB is somewhat deceptive insofar as a part of the debt securities to be issued by the former will end up on the balance sheet of the latter, so that one should avoid double counting. In its commendable efforts to keep interest rates low and avoid impairing corporations' ability to raise equity, the ECB has chosen to ignore the long term fallout of this debt explosion ; it comes on the back of already record levels of public and private debt and could lead, in due course, to rekindling inflation and higher rates of interest. These problems have been deliberately side-lined in light of the developing economic crisis and its potential dramatic consequences in both social and political terms; these unprecedented recovery measures, for which the authorities do not appear to receive the necessary credit, are in fact amply justified.

The borrower:

For maximum transparency and in order to achieve broad acceptance by investors, it is highly preferable that the borrower be the "European Union" itself. The Union is a "legal entity" (which was not the case in the 1990's when it was necessary to resort to the "European Community") which allows to dispense with the creation of a special purpose borrowing vehicle which, in turn, would have needed an EU budget guarantee to ensure its credibility. Indeed the treaty itself requires the EU budget to be in equilibrium which, by construction, confers on its obligations the "joint and several guarantee" of the Member States, justifying the EU's coveted AAA rating.

|

|

The budget:

Every budget is made up of "resources and expenditures". Whether it concerns the Union's plurennial financial perspectives or the annual operating budgets, the treaty imposes that they are always balanced, meaning that any deficit must be covered by the MS. Another important distinction is to be made between the "authorized operating budget" proposed by the Commission and approved (before each 7 year cycle and annually) by the Council (requiring unanimity) and the EP (requiring a simple majority) and the "execution of the budget" which accounts for the actual execution and legal commitments entered; reallocation of funds between budget lines is authorized (Bourlanges procedure); under-execution of the budget leads to carrying forward all legal commitments entered into and the cancellation of the balance which is returned to the MS.

a. Expenditures

They are divided in a series of Chapters which, in turn, are subdivided in "budgetary lines", each of which is accompanied by a description of its objectives and of the modalities/conditionality of access. It is perfectly possible, for ease of supervision, to consider the recovery plan as a specific Chapter of the budget, divided into a series of programs, each represented by a specific budget line with among their specifications, whether disbursements will be in the form of grants or loans and under what conditions.

With regards to loans, it is important to understand that the role of the EU in deploying this new instrument is fundamentally different than the one it played when its function was to act as a mere intermediary between the market and third party beneficiaries: in that situation, the terms of the issue on the market and those of the loan to the beneficiary were simply back to back with the risk taken by the EU limited to the solvency of the borrower, transferring to the beneficiary the full benefits of the EU's more favourable market acceptance.

This template is not applicable to the € 250 billion of borrowings proposed which must remain entirely separate from the many independent loans they will be financing. Indeed, without this specification, unacceptable inequalities would appear between terms granted to MS, based simply on market fluctuations during the 7 year disbursement period. It should be up to the budget to assume the terms and conditions of its borrowings independently of their affectation (see further down under Rates and early Redemption for ways to mitigate this risk). It behoves the Commission to offer identical conditions to MS subject only to the maturity of the loan granted and of other "objective" criteria (as detailed in the commentary of each budget line).

b. Resources

They can be divided into three categories: 1) MS direct contributions, 2) Own resources (taxes and revenues accruing directly to the EU) and – in the future – 3) The proceeds of borrowings on the financial markets. Their total should equate the expenditures budgeted in the corresponding year; among these categories, the first serves as the balancing item: the greater the EU's own resources and the proceeds of its borrowings, the lower will be the calls on MS contributions.

With regard to the EU's own resources, Ursula von der Leyen mentioned the need to broaden their existing base, suggesting a number of possibilities which have already been examined in the past but so far to no avail. It would appear that her aim is to raise sufficient funds to cover all or part of the EU's future "debt service" needs.

The issuance of bonds is more a complex question and deserves closer scrutiny.

|

|

Amount: The proposal suggests a maximum amount of € 750 billion in tranches (not necessarily equal) over the full period of the financial perspectives.

Maturities: The proposal suggests issues of maturities covering the full spectrum of the yield curve up to 30 years with repayments between 2027 and 2058.

Several financial commentators, among whom George Soros, have suggested that the EU should contemplate the issuance of perpetual bonds (whose service is limited to the interest coupon). While this idea seems particularly appealing in a low interest rate environment, I believe that this is a "false good idea" for the following reasons: first, there is no indication of the capacity of the market to absorb large quantities of such securities; second, the interest rate premium demanded by investors might be substantial for market rather than solvency risks; finally, as soon as interest rates rise - even in a few years' time – the bonds will trade at a corresponding steep discount, giving a poor image of the issuer and inhibiting the EU's capacity to issue new tranches on acceptable terms.

Interest rates and early Redemption: In order to guarantee the EU's access to financial markets on optimal terms and reduce over time the impact of interest rate fluctuations, I will repeat a previous suggestion made in my April 18tharticle ("The EU is the correct level to implement the recovery program after Covid19"). Starting from the observation that long term interest rates for the strongest Eurozone Members hover around 0% and that these same Members guarantee – through the treaty – the securities to be issued by the EU, the latter should be able to borrow on similar terms, i.e. around 0%.

Nevertheless, in order to ensure the stability of their value – independently of interest rate fluctuations - Member States would undertake to accept these securities - at their face value - in payment of any fiscal debt owed by its owner to the national government. In turn, direct contributions of MS to the EU budget could be discharged by presenting the securities that they may have acquired through this process.

These particular characteristics confer on the securities a constant value close to par, as they can be considered a "cash equivalent", regardless of their stated maturity. Thus, no coupon would be attached to any present or future EU bonds, an issue price above or below par being able to account for fluctuations of money market rates (as is the case for US T-bills). This instrument would be particularly attractive to banks as a safe substitute for deposits with the ECB on which they currently pay interest for the privilege.

Securities received from the MS by the budget would be cancelled (reducing the EU's outstanding debt). The "maximum authorized level" (initially € 750 billion) of outstanding debt would be determined by the European Council and the PE, at each renewal of the financial perspectives (as is the case from time to time by the US Congress). As long as the outstanding debt remained below the ceiling, the EU could continue to borrow, reducing its need to call on MS direct contributions.

Such a system would entail setting up a "debt management office" either within the Budget Directorate General of the Commission or independently thereof; the financial regulations of the EU would need to be amended accordingly.

Conclusions:

As soon as a sufficient EU securities were outstanding, a deep and liquid secondary market would develop because, even if stated maturities differed, all securities would be de facto "fungible", because useable at any time at their face value.

|

|

This characteristic would provide the ECB with a powerful tool to regulate the monetary market by buying or selling securities to provide or withdraw liquidity from the market, in the same way as the FED does in the USA. In addition the financial market would finally have access to an undisputed "safe asset" which could be used as benchmark, the lack of which currently penalizes severely the development of the € denominated financial market.

This development would, in addition, contribute powerfully to the sustainability of the Single Currency, compensating MS for their loss of autonomous control over their exchange rate (as is the case for the 50 U.S. federated States). It should also lead to an accelerated extension of the Eurozone to all 27 MS and reinforce the competitivity of the € versus the USD in both international financial and commercial markets. The EU would considerably increase its weight on the geopolitical stage at a time when American and Chinese domination are increasingly marginalizing the EU's position.

Though it appears prudent to limit the new budgetary proposals of the Commission to the funding of the recovery program, in order not to provoke unnecessarily the opposition of the so-called "frugal" countries and of all "national-populist" parties, nothing should prevent, over time to expand the system the financing of the entire EU budget. Creating greater flexibility and solidarity by focusing more on shared rather competing interests of its citizens would contribute to reducing, through the budgetary transfer mechanism, the trend towards increasing inequalities that threaten the cohesion of the EU. This could turn out to be the trigger leading to the creation of a truly European "demos" which remains to date an impossible dream.

Implementing the Commission's proposal would establish the basis for the EU's own "sovereign debt", relying on the wealth of all its 27 Members. The capacity to finance in the long run the entire budget by relying exclusively on its "own resources" and "debt issuance" seems considerable: indeed if one compares the US Federal debt (exceeding at present $ 22.8 trillion) to that of the EU (currently negligible) and if one considers that the debt of the U.S. federated States as equivalent to the total sovereign debts of the MS, one can easily conclude that their remains a vast amount of untapped resources; its mobilization over the next 30 years and beyond could allow the EU to close the gap in sectors such as digital sciences, AI, investment in infrastructures, health, environment, defense, etc.

These are the reasons why particular attention should be given to the long term implications of the agreements resulting from the forthcoming negotiations and refuse any compromise that might become an obstacle to the Union's further integration.

The solidarity implicit to the implementation of such a program is precisely the reason that it will prove highly controversial; it would, indeed, be a major blow to the hopes of all nationalist and populist parties who are brazenly capitalizing on the pandemic to extoll the virtues of a largely outdated and inefficient concept of "national sovereignty". It is important to understand that, underlying the arguments criticizing the Commission's proposals, lurks a visceral resistance of many MS (and of national-populists parties in particular) to see any transfers of powers to "Brussels" to the detriment of their respective prerogatives. The adoption of the Commission's proposals is an inescapable precondition to deal successfully with the oncoming crisis; at the same time it should, accelerate the need for Treaty change conferring added purpose to the forthcoming "Conference on the future of Europe".

Now is the occasion and obligation– for each Member State – to decide on its own future within or outside of the European project." |