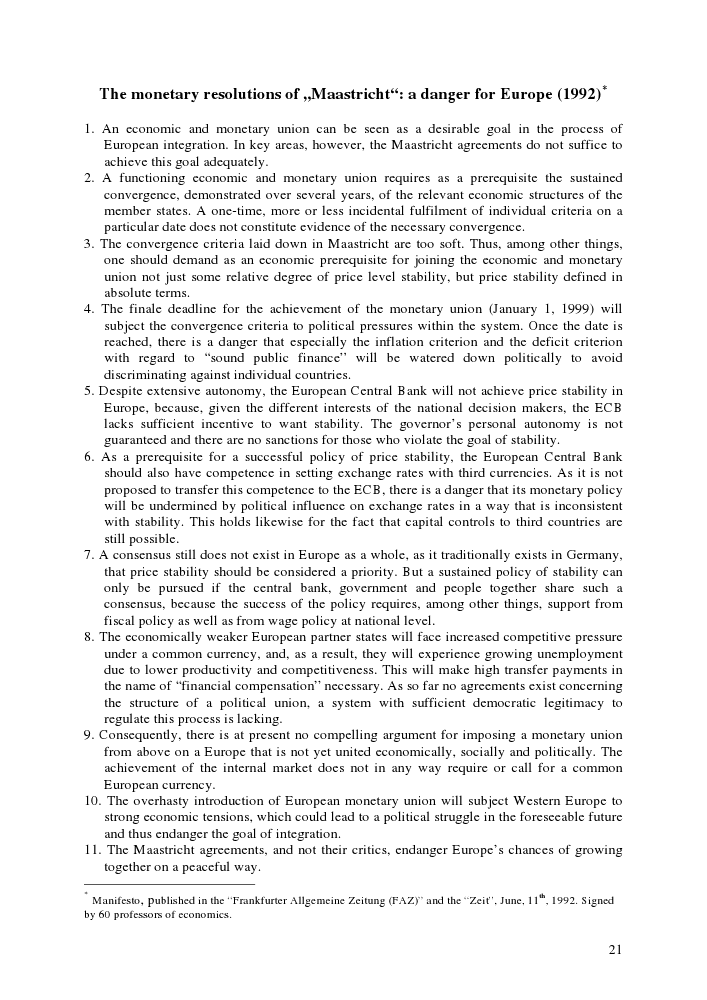

The euro was launched 15 years ago through the Maastricht Treaty, and was expected to make Europe stronger economically and more integrated. Although the Delors report in 1989 correctly identified many of the structures needed to make EMU work, the Maastricht design underplayed the importance of labour and product flexibility, and of divergences in competitiveness. For most of its first decade the euro area grew quickly, coinciding with a period of very rapid world growth. However, the global economic and financial crisis that started in 2007 hit Europe hard, exposing serious flaws in its original design. Although the crisis began in the United States, Europe ended up being the worst-affected region. At one point, markets and commentators began to ask serious questions about whether the single currency could survive. Important measures were taken to save the euro, and since 2012 markets have become calmer, as European leaders and policy-makers signalled they were prepared to take tough decisions. In particular, the president of the European Central Bank (ECB), Mario Draghi, promised to do ‘whatever it takes’ to protect the euro.

The Chatham House, Elcano and AREL Report by

Stephen Pickford, Federico Steinberg and Miguel Otero-Iglesias from March 2014, 'How to Fix the Euro. Strengthening Economic Governance in Europe', examines why the economic and monetary union (EMU) was so badly affected by the crisis, and assesses whether further changes need to be made to the structure of economic governance that underpins it.

Paul N. Goldschmidt, Director, European Commission (ret.); former Member of the Steering Committee of the Thomas More Institute, distributed an article entitled 'The ECB and austerity': As the forthcoming European elections approach, it is urgent to clarify the debate surrounding the ECB so as to avoid that simplistic and superficial slogans propagated by overzealous politicians misinform the elector. Indeed, many voices are suggesting that excessive (budgetary) austerity is counterproductive and capable of stalling the nascent economic recovery. These criticisms refer to declarations by personalities such as Christine Lagarde (IMF) or number of recognised economists – whose views are often misinterpreted or taken out of context – when they are not simply the ructions of politicians vaunting inapplicable measures such as “eurexit”, salary increases, protectionism, postponing budgetary rigour, etc. The debate would be, in part, more seriously grounded if, as is the case in Italy, the projected stimulus is accompanied by ambitious structural measures subject to a rigorous timetable (imposed under the threat of the government’s resignation) or recognises the impressive and painful reforms already implemented (Greece, Ireland, Portugal Spain); on the other hand it is not acceptable in the French case where the request for further European “indulgence” aims at obfuscating the dissensions within the governing majority allowing, once again, to postpone unpopular decisions.

There seems to be a broad consensus on the diagnosis which, in the absence of an agreement to reduce national deficits, aims, nevertheless, at reducing excessive indebtedness (lip service to the burden on future generations). This stance is structurally contradictory unless an EMU wide agreement to devalue the debt through inflation was achievable, which is clearly utopian. So the protagonists fall back on the easy way out by conferring on “Europe” the responsibility for stimulating economic growth while, simultaneously, denying it the necessary resources. Indeed, it is only at European level that a policy aiming at stimulating consumption in “healthy” Member States (Germany) can be envisaged so as to attenuate the impact of austerity measures on countries that have not yet even started to implement seriously the required structural reforms (France).

The preferred scapegoat of supporters of a European stimulated growth policy is the ECB whose independence is strongly contested in this particular regard. It is invited to finance the recovery through measures that would, if necessary, totally disregard its by-laws and/or the EU Treaties. Such a choice comes easily as it appears to exonerate national governments despite the fact that, together with their predecessors, they alone are responsible for drafting and ratifying the Treaties and Regulations that “Brussels” and “Frankfurt” are charged with implementing.

Any objective analysis would conclude that the ECB has already interpreted the rules that govern its operations with a significant degree of flexibility (enough to anger the Bundesbank) and, in so doing, can also claim to have, so far, done “everything it takes to save the €”. If the EMU’s monetary policy, implemented by the ECB, constitutes an important aspect of economic policy, it is, nevertheless, obvious that it cannot, in and of itself, be the sole spur to the recovery.

Thus, the ECB finds itself alone in imagining new tools to carry out monetary policy within the Eurozone. These concern principally “quantitative easing” which, as clearly explained by President Draghi, must take into account the structural differences between credit markets in the Anglo-Saxon world (based on capital markets financing) and in the Eurozone (based on bank financing), a fact that largely escapes the understanding of politicians. Furthermore, while in the United States and England, their respective Central Banks dialogue with governments disposing of significant resources and budgets, the ECB has no legitimate interlocutor with which it can coordinate its interventions. Indeed this “Europe” that is supposed to finance the recovery is prohibited by the Treaties to indulge in monetary financing; additionally, by a unanimous decision of the Member States, it is endowed with an insignificant budget and derisory “own resources” limiting any significant recourse to issuance of Eurobonds, project bonds, etc. which, otherwise, might be eligible for purchases by the ECB, on the model of the American Federal Reserve Bank or the Bank of England.

It should be perfectly obvious to any good faith observer that, within the framework of the current Treaties, any direct financing by the ECB of Member State’s deficits is impossible to implement without incurring important moral hazard risks; to avoid them, it would be necessary to frame such a policy very strictly which would be tantamount to reinstituting the provisions that are already in force in the Stability and Growth Pact, the Budgetary Treaty, the Six and Two Packs, which together – oh surprise – are precisely the safeguards Member States imposed for any recourse to the European Stability Mechanism!

It is clearly highly desirable that, one day, the ECB will be endowed with similar powers to those at the disposal of their American, British of Japanese counterparts in the financing of the economy as well as intervening efficiently in foreign exchange markets. This implies further integration towards a “federal” Eurozone and therefore a thorough revision of the Treaty, which is currently not on the cards.

Calling for further ECB intervention and purporting that it constitutes the panacea countering the need for austerity and structural reforms is a gross lie. It is being propagated not only by nationalist/populist Europhobic parties but equally by number of alleged Europhile members of government majorities who are always keen to ask of Europe what it cannot deliver because they refuse systematically to provide it with the necessary resources. |

{kind=link}

{kind=link}